- 债券基金类型

债基/ˈbɒnd fʌnd/常见为政府债、投资级、非投资级与多元收益;费用率低、流动性好。

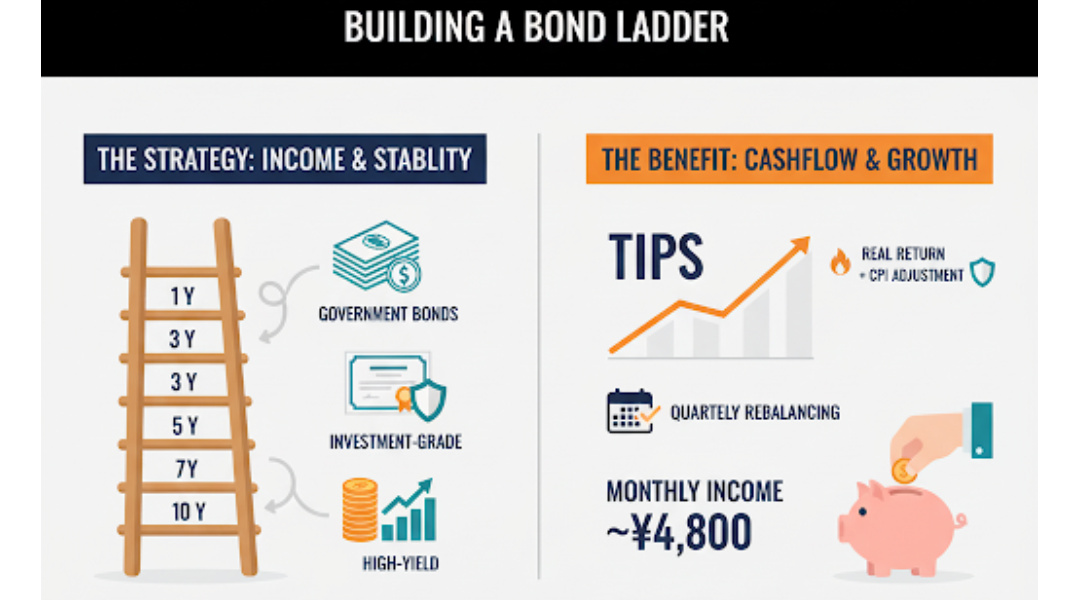

/ˈbɒnd fʌnd/ types: government, investment-grade, high-yield, multi-income; low fees, good liquidity.

为什么用“期限阶梯”

/ˈlӕdər/阶梯用1–3–5–7–10年分布,降低再投资风险、减少利率错配,锁定滚动到期现金流。

A /ˈlӕdər/ spreads 1–3–5–7–10Y maturities, cutting reinvestment risk and rate mismatch, locking rolling cash flows.

TIPS的作用

TIPS/ˈtɪps/将本金随CPI指数化,提供“真实收益+通胀补偿”,在通胀抬头期稳定购买力。

TIPS /ˈtɪps/ CPI-index principal, delivering real yield + inflation uplift, stabilizing purchasing power.

示例配置与现金流

核心60%阶梯国债基金,卫星25%高收益债,15% TIPS;以¥120万投入,年化4.8%,税前月流入约¥4,800。

Sample: 60% laddered treasuries, 25% high-yield, 15% TIPS; invest ¥1.2M, 4.8% p.a., ~¥4,800/month pre-tax.

实施与再平衡

每季检查权重偏离≥5%即调仓;高收益债占比随年龄递减,退休后提高阶梯权重。

Rebalance quarterly on ≥5% drift; taper high-yield with age, raise ladder in retirement.

FAQ

- 与定存相比优势?

可交易、潜在更高收益、税务与通胀效率更好。

- Versus time deposits?

Tradable, higher yield potential, better tax/inflation efficiency.

- TIPS会亏吗?

实质利率上行时价格波动,但本金随CPI调整。

- Can TIPS lose?

Prices swing as real rates rise; principal adjusts with CPI.

- 外币风险怎么管?

选本币对冲级别ETF或本币债基金。

- FX risk?

Use local-currency hedged ETFs or local debt funds.

- 高收益债违约怎控?

限仓25%内,分散行业,偏BBB-至BB。

- HY default control?

Cap ≤25%, diversify, tilt BBB– to BB.

- 何时加仓/减仓?

利率见顶期加阶梯,经济放缓期降高收益。

- When to tilt?

Add ladder near peak rates; trim HY in slowdowns.

- 税务注意什么?

关注利息所得税与基金分配规则。

- Taxes?

Mind interest income tax and distribution rules.

关键词

- 中债券基金,期限阶梯,TIPS,固定收益,通胀对冲,再投资风险

- bond funds, maturity ladder, TIPS, fixed income, inflation hedge, reinvestment risk